In this article Martin Shaw, Chief Executive of the Association of Financial Mutuals, takes an in-depth look at the current state of the With-profits market and asks the question if now is the time to consider them for your clients.

As one of the UK's leading With-profits providers we obviously believe it is but ultimately it's for advisers to make an informed decision about what's best for their clients.

The following article appears in the August edition of Mutually Yours the newsletter of the Association of Financial Mutuals and is reproduced with their permission. ![]()

How with-profits funds help investors weather stormy markets

In Q2 2020, the UK stock market grew 9 per cent. Despite that, year to date, the market was still down 18%. Volatility in the value of shares has grown significantly in recent years because markets are able to respond more quickly to worldwide events with the advent of 24-hour news and because sentiment seems to be changing more quickly than the weather. And it’s not just coronavirus that markets are having to factor in: the post-Covid recession, Brexit and the US elections are changing investor perceptions daily, as indeed is the weather (or at least climate change).

For the average cautious investor or pension trustee, the level of volatility in the market is a major turn-off. The last time we saw such adverse conditions for investing, in 2008/09, people turned to safe havens such as cash, government bonds- and yes, with-profits.

During the financial crisis of 2008/09, many AFM members showed record sales volumes. People saw mutuals and friendly societies as a safe pair of hands and, in particular, customers for whom with-profits savings were appropriate valued the capacity of the product to smooth out the peaks and troughs of the market.

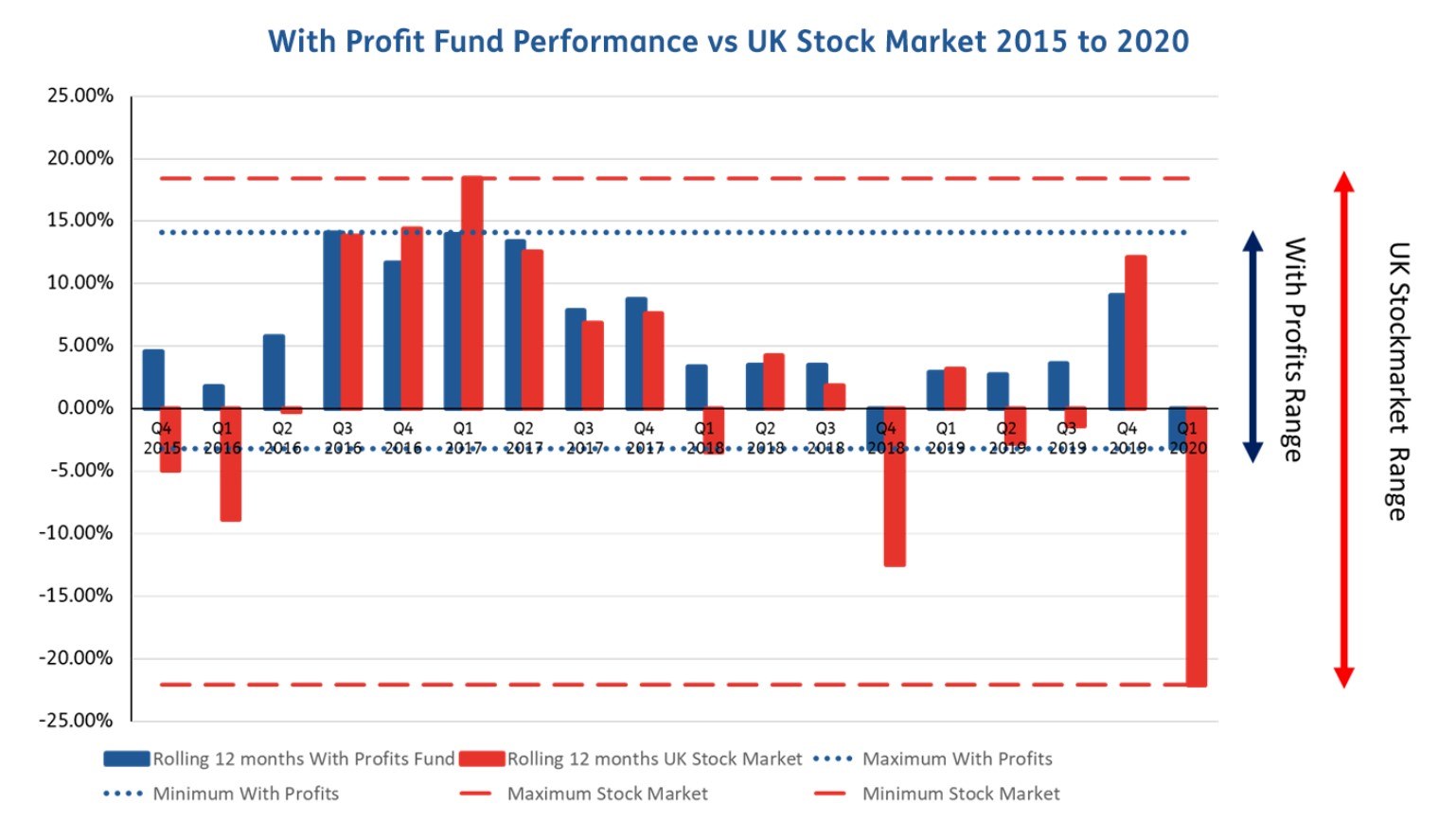

As the chart below shows, based on analysis by a member of AFM, over the last five years the UK stock market has, on a rolling 12 months basis, reported negative quarters almost as often as it has positive (8 quarters versus 10). This compared to just two negative quarters for with-profits and 16 positive. Furthermore, in only 5 of the 18 quarters did the market outperform with-profits.

With regard to volatility, as the chart also demonstrates, the range of quarterly performance for the stock market, between +18% and -22%, is more than twice as great as that for with- profits. This of course means that for the cautious investor, a with-profits product offers a much less volatile option.

There are two main features of a with-profits product that allow for this more reliable performance: the allocation of bonuses, and smoothing. In a with-profits product, the provider declares a bonus rate each year; once a bonus is declared it cannot be taken away as long as the customer maintains the contract up to maturity. Smoothing means that the provider will set the rate of bonus by taking a long-term view, rather than simply reflecting the most recent performance of the underlying investments.

There are other features of a with-profits product that help reduce volatility: first, the product can invest in a wide range of assets, including bonds, gilts and property, not just the stockmarket and that diversity helps offset market falls; second, when the product matures, the provider may pay a terminal bonus in addition to the annual ones; and third, the with- profits product may feature a guarantee, meaning that at the end of the term, or on death before maturity, a specified sum will be payable.

It would also be remiss of me not to mention that, in absolute terms, with-profit policies invested with a mutual insurer or friendly society have, according to AFM research, provided investment returns much greater than an average unitised product with a similar structure.

As a result, with-profits are particularly worth considering for investors with a set time frame in mind or a long-term view; for example, planning for retirement or paying for a child’s education, as they would potentially benefit from the more predictable and superior returns offered.

People with a long memory may recall the concerns around with-profits as a result of the mis-selling of mortgage endowments in the last century and the failure of Equitable Life in 2000. However, since that time, the degree of regulation has intensified significantly and with-profits providers need to set aside enough capital to cover all their liabilities, as well as to allow for one-in-two hundred year events (which seem to be happening quite a lot lately). There is also a high level of transparency in the way the product is managed and boards are subject to extensive governance requirements.

According to a report issued last year by FCA, at the end of 2017 there was around £247 billion invested across 14 million with-profits policies. Whilst this had fallen from a peak of over £400 billion, as FCA stated, it still represents a "significant portion of the long-term savings, pension and retirement income provisions of customers in the UK".

We can expect further turbulence in the stockmarket in coming months and investors will be wary about the prospects for their portfolio. By ensuring with-profits makes up part of their assets, they can continue to enjoy growth when the markets are high, and suffer less in the downturn.

With-profits truly is a fund for all seasons.